As we sat down to do our monthly budget at the beginning of the month, I had a thought.

I should share this with people! Not because my budget looks amazing or to show off how much I make (cause you would just laugh). But rather, to share how it works and how we thrive using it! (Because surprisingly, we do!)

The idea of a budget is to not only know where your money is going but to

decide where it goes. You have the power here, not your money or your bills. The goal of a budget is to keep your expenses below your income so a) don't go into debt and b) can start saving.

It took us several months to get used to having a shared income, knowing how much we should budget for everything, and felt totally comfortable with it (aka new what we were doing). But once we got there, we loved it! It doesn't feel as restrictive as I thought "budgeting" would. Do I dare say it is freeing? Invigorating? Yes, I get that excited about my budget.

Anyway, I'd like to share what we do in case it would help someone out there.

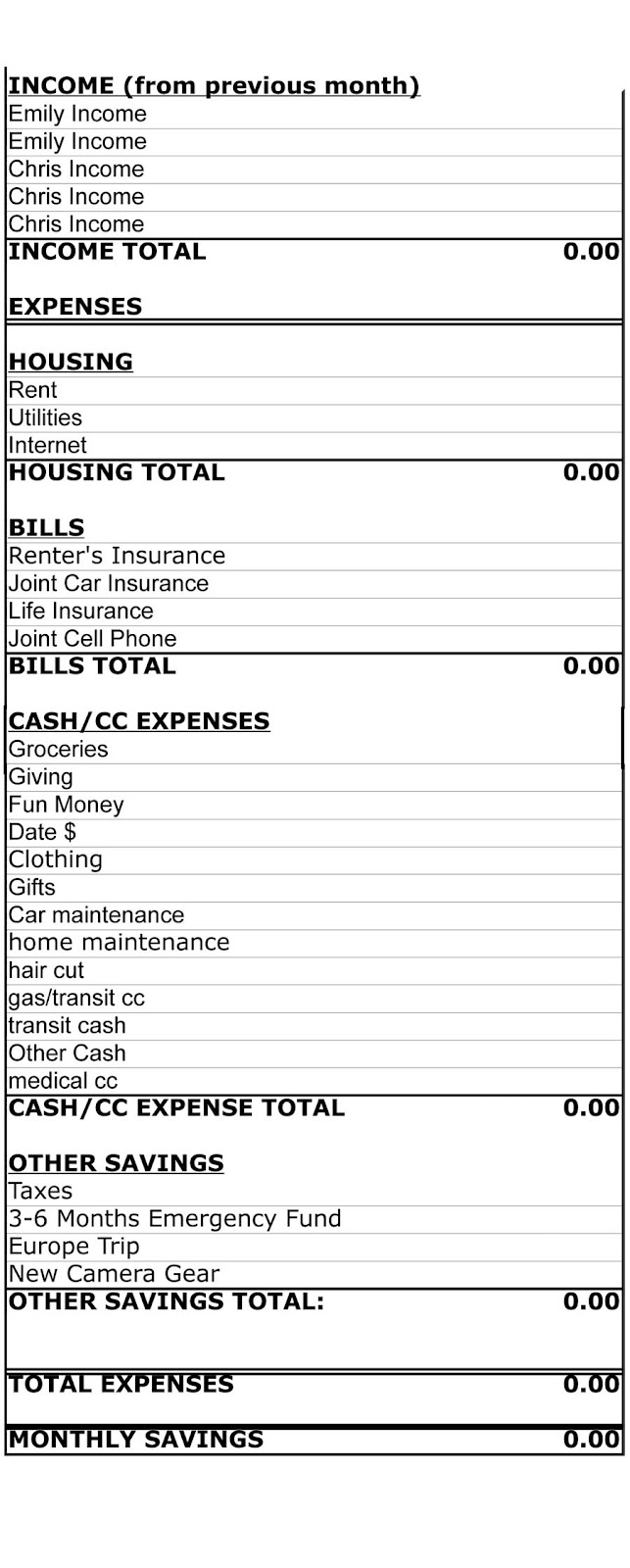

Chris created a spreadsheet where we keep track of our income and plan out our expenses:

- At the top, we enter in our income. (Each paycheck on a separate line then totaled below that.) I should note that we use the income from the previous month not the upcoming month's paychecks. For example: In March we each had two paychecks, those went into our April budget. It may take a while before you can do this 100% but I would recommend it. That way you are only spending money you know you have (especially important when one of you works by contract).

- Then begins the list of our expenses. These are broken up into three sections: Housing (rent, utilities, internet, etc. ) Bills (you know the ones you have every month), and Cash/Credit Card expenses (this includes everything else)

- The next section is Savings. We have several things we are saving up for all the time - emergency savings, a trip to Europe, camera equipment, a new bike, etc. Every month we decide which savings fund gets money, which ones don't and if our goals need to be changed.

- Then at the bottom of the spreadsheet we have the outcome: Income Total - Expense Total - Savings = Left Over Savings (We try not to let this be too high because we have all of our savings listed above it, but this will tell us how much we have left over . . . or if we went beyond our income . . . in which case we need to revise the budget).

Now for the fun part: Spending money!

Chris and I use the cash-envelope system for most of the items in the Cash/Credit Card category. Again, this takes time to get used to but is definitely worth it. This is by far the easiest way to stick to your budget . . . if the envelope is empty you can't spend it! It also reinforces that YOU are in charge of YOUR money. You decide how that cash is spent. You start questioning your decisions a little more. "Do I really need to eat out again? Is this shirt really worth $__. If I buy this now, I won't have enough for ___." You get the idea. When we stop asking ourselves these questions, that's when we pull out the credit card and go into debt. That is not an option for us.

Some envelopes accumulate money month after month. Like my clothing envelope. I don't buy clothes every month which works out well because then when it's time for new running shoes, I have enough money ready to pay for them. Our car and home maintenance funds accumulate too because you never know when you need to make a larger purchase or repair. For our hair cut budget, we only put in a third of the cost of the hair cut each month and that way every three months we can get a hair cut (this helps so you only take a small sum each month instead of a large sum once every three months). But our grocery budget gets used up every month . . . and that's how that envelope should work. Our fun money varies every month; sometimes I go through it in the first week (which is too bad for me), but other times I have a lot left over and can use it however I want in the following months.

Some purchases are made with the credit card and we do use it for online purchases, too. But that is either already allotted in our budget (like automatic donations or medical bills) or paid back with cash from the respective envelope.

When the month is over, we go back through the budget and see how well we did. What did we overspend on (unexpected trips or visitors) or what money didn't get used. This helps us know if we need to be adjusting our budget for the next month. When gas prices went up and Chris had a longer commute for one of his projects, our gas/transit budget was way off! But we adjusted it for future months and now it hasn't been a problem.

I hope this was helpful to some of you. Creating a budget, learning to live below your means, and sticking with it are worth all the effort I promise! There are so many resources out there for creating and following a budget. This is what works for us. I'd love to hear what works for you! And if you have any questions, please ask! I

love talking about budgets, saving and financial freedom.

As we sat down to do our monthly budget at the beginning of the month, I had a thought.

I should share this with people! Not because my budget looks amazing or to show off how much I make (cause you would just laugh). But rather, to share how it works and how we thrive using it! (Because surprisingly, we do!)

The idea of a budget is to not only know where your money is going but to

decide where it goes. You have the power here, not your money or your bills. The goal of a budget is to keep your expenses below your income so a) don't go into debt and b) can start saving.

It took us several months to get used to having a shared income, knowing how much we should budget for everything, and felt totally comfortable with it (aka new what we were doing). But once we got there, we loved it! It doesn't feel as restrictive as I thought "budgeting" would. Do I dare say it is freeing? Invigorating? Yes, I get that excited about my budget.

Anyway, I'd like to share what we do in case it would help someone out there.

Chris created a spreadsheet where we keep track of our income and plan out our expenses:

- At the top, we enter in our income. (Each paycheck on a separate line then totaled below that.) I should note that we use the income from the previous month not the upcoming month's paychecks. For example: In March we each had two paychecks, those went into our April budget. It may take a while before you can do this 100% but I would recommend it. That way you are only spending money you know you have (especially important when one of you works by contract).

- Then begins the list of our expenses. These are broken up into three sections: Housing (rent, utilities, internet, etc. ) Bills (you know the ones you have every month), and Cash/Credit Card expenses (this includes everything else)

- The next section is Savings. We have several things we are saving up for all the time - emergency savings, a trip to Europe, camera equipment, a new bike, etc. Every month we decide which savings fund gets money, which ones don't and if our goals need to be changed.

- Then at the bottom of the spreadsheet we have the outcome: Income Total - Expense Total - Savings = Left Over Savings (We try not to let this be too high because we have all of our savings listed above it, but this will tell us how much we have left over . . . or if we went beyond our income . . . in which case we need to revise the budget).

Now for the fun part: Spending money!

Chris and I use the cash-envelope system for most of the items in the Cash/Credit Card category. Again, this takes time to get used to but is definitely worth it. This is by far the easiest way to stick to your budget . . . if the envelope is empty you can't spend it! It also reinforces that YOU are in charge of YOUR money. You decide how that cash is spent. You start questioning your decisions a little more. "Do I really need to eat out again? Is this shirt really worth $__. If I buy this now, I won't have enough for ___." You get the idea. When we stop asking ourselves these questions, that's when we pull out the credit card and go into debt. That is not an option for us.

Some envelopes accumulate money month after month. Like my clothing envelope. I don't buy clothes every month which works out well because then when it's time for new running shoes, I have enough money ready to pay for them. Our car and home maintenance funds accumulate too because you never know when you need to make a larger purchase or repair. For our hair cut budget, we only put in a third of the cost of the hair cut each month and that way every three months we can get a hair cut (this helps so you only take a small sum each month instead of a large sum once every three months). But our grocery budget gets used up every month . . . and that's how that envelope should work. Our fun money varies every month; sometimes I go through it in the first week (which is too bad for me), but other times I have a lot left over and can use it however I want in the following months.

Some purchases are made with the credit card and we do use it for online purchases, too. But that is either already allotted in our budget (like automatic donations or medical bills) or paid back with cash from the respective envelope.

When the month is over, we go back through the budget and see how well we did. What did we overspend on (unexpected trips or visitors) or what money didn't get used. This helps us know if we need to be adjusting our budget for the next month. When gas prices went up and Chris had a longer commute for one of his projects, our gas/transit budget was way off! But we adjusted it for future months and now it hasn't been a problem.

I hope this was helpful to some of you. Creating a budget, learning to live below your means, and sticking with it are worth all the effort I promise! There are so many resources out there for creating and following a budget. This is what works for us. I'd love to hear what works for you! And if you have any questions, please ask! I

love talking about budgets, saving and financial freedom.

3 comments:

Emily, this was a really interesting, and for me, appropriate post. I have never really used a budget that is actually written up. I always just kind of had a general idea of how much I had to spend. But now, my income will be much lower, so I've decided that I need a budget. My only concern is how to "restrict" my spending. I'm not really a fan of the envelope method mainly for convenience reasons, but I can see how that would be a good, tangible way to let yourself know how much you can spend. Do you take the envelopes with you whenever you leave the house, or do you just take out the amount you think you'll need? To me, I think it would be easier to just keep a running balance of how much is in each spending account, but I'm not sure I'd remember to write down each purchase when I make it. Thoughts?

I always like to talk about budgets and finances. I'm getting married here in 2 months and budgeting for the wedding get seemingly difficult as you have 2 people spending money and 2 people with income. I really like the idea of using the previous months income. For us though I dont think I could go to a pure cash system like you. I use to have alotted $16/day for whatever I wanted to spend it on (gas, food, fun, anything) The money accumulated so to fill up my car I would wait a couple days.

Now with 2 people it is getting more challenging, but what I have found is similar to what you have only a little more techy... There are budgeting apps out there that will sync with 2 different phones and we can have as many different budgeting categories such as groceries, mortgage, out to eat, etc and you can manually add money to these "mini" budgets or have them automatically scheduled to increase... then if there is not enough money in the "mini" budget you cannat purchase what you want

Interesting Read

Thanks Emily

Matt Nelson

Hi AllieCat - I also have tried the "general idea" model of budgeting and found it didn't make me accountable to anything! I've also gone through a phase of writing down each purchase under a category, but that was tedious and often forgotten. I think having a written out budget made me accountable, and using cash just added to the accountability. A budget needs to sync well with your priorities and be realistic for your lifestyle and income--otherwise it won't work. It's not something you want to "fight against." For your question for the envelopes, I just take the cash I will need for that day or week with me and keep them separate in my wallet with dividers. I always have a little bit of "fun money" on me though - just in case!

Post a Comment